The U.S. M&A Market in 2025: Trends, Deal Activity, and Strategic Outlook

- Jun 1

- 2 min read

Every cycle in dealmaking is shaped by forces that few notice until they have already moved the market. Interest rates, antitrust posture, the political color of regulatory agencies — these are the invisible currents that decide whether a year produces $50 billion in fintech transactions or $200 billion. 2025 was one of those inflection years, and most observers spent it looking at deal headlines instead of the policy machinery underneath.

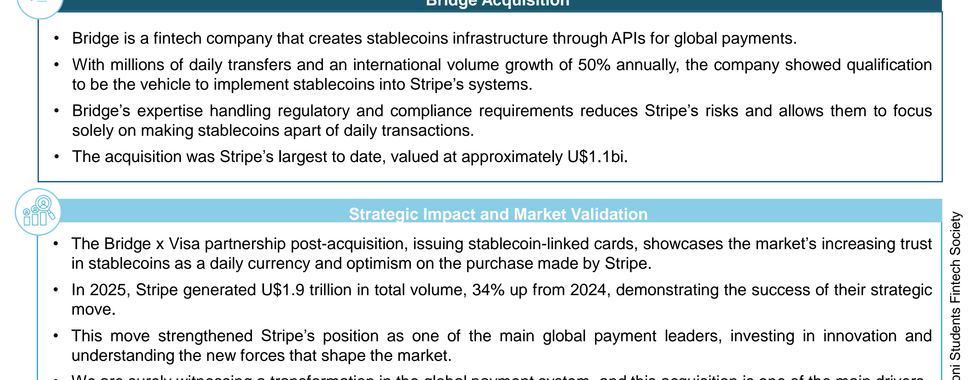

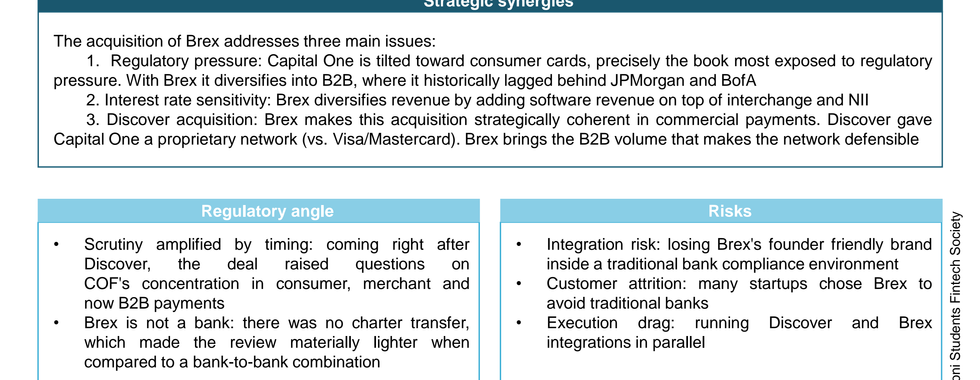

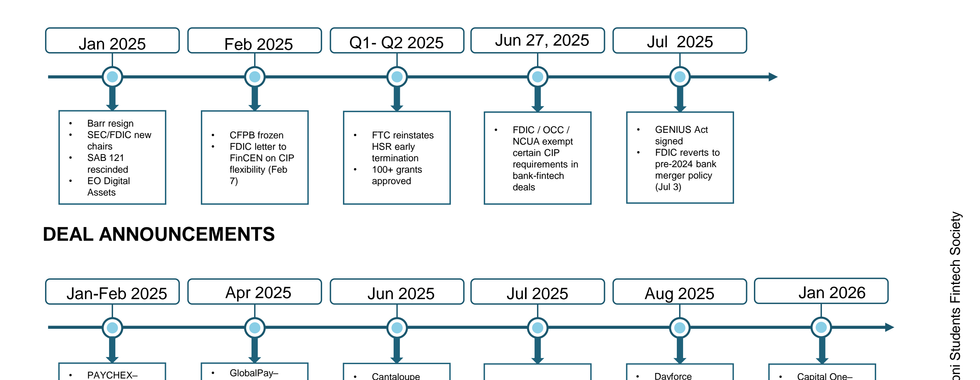

Within twelve months, the United States rewrote the rulebook for financial M&A. The CFPB was effectively frozen, the FDIC reversed its 2024 bank merger policy, the SEC rescinded SAB 121 and opened the door to bank-crypto integration, the FTC reinstated HSR early termination on more than 100 deals, and Congress passed the GENIUS Act — the first federal stablecoin framework in American history. Three to six months later, exactly as deal preparation cycles would predict, transactions began clustering: Stripe–Bridge, Capital One–Brex, Global Payments–Worldpay, Thoma Bravo–Verint, Centerbridge–MeridianLink. The market did not get lucky. It got permission.

Our report, The U.S. M&A Market in 2025: Trends, Deal Activity, and Strategic Outlook, traces the line from political signal to deal timing. We dissect the regulatory shifts of Q1 2025, map them against the deal announcements that followed, and break down the transactions that defined the year — what was paid, what was acquired, and what each acquirer was really buying when the headline said "fintech." We examine why valuations compressed even as deal volume recovered, why corporate venture capital surged to $56.7 billion despite fewer transactions, and why the next phase of consolidation will be fought over regulated infrastructure and AI capability stacks rather than user growth.

This is not a story about deregulation versus regulation. It is a story about how capital reorganizes itself the moment uncertainty lifts — and about the strategic logic that emerges when incumbents realize they can no longer build the next generation of financial infrastructure organically. The question is no longer whether the M&A market has reopened. It has. The question is who will own the rails when it closes again.

This is why the Bocconi Students Fintech Society has made the 2025 U.S. M&A landscape the focus of this report: because understanding the policy-to-deal transmission mechanism is the difference between reading the market and being moved by it

Slide Deck

Read the Slide Deck below ⬇️

Download the Slide Deck below ⬇️

Published in June 2026

Project Team

Project Leader: Musat Andrei David

Junior Analysts: Niccolo Graziani, Felipe Waddington Achatz, Federico Corda, Darien Weber, Anthony Kozlowski, Maria Eduarda Moraes, Gabriele Surijon, Rudolf Hozmann, Enrico Fabri

Association Board :

Neil Maaouni (President & Head of Data Analysis), Mathilde Castagine (Vice President & Head of Events), Guillaume Abaz (Senior Advisor to the board), Andrea Botero (Head of M&A and VC), Antonina Bojanowska (Head of Generalist), Noé Wierzba (Head of Operations), Lucas Médina (Head of Corporate Analysis) , Alexandra Minca (Head of Communication)

Comments